Choosing your accounting basis when setting up ExpensePlus

This article explains how to set up your accounting basis when setting up ExpensePlus.

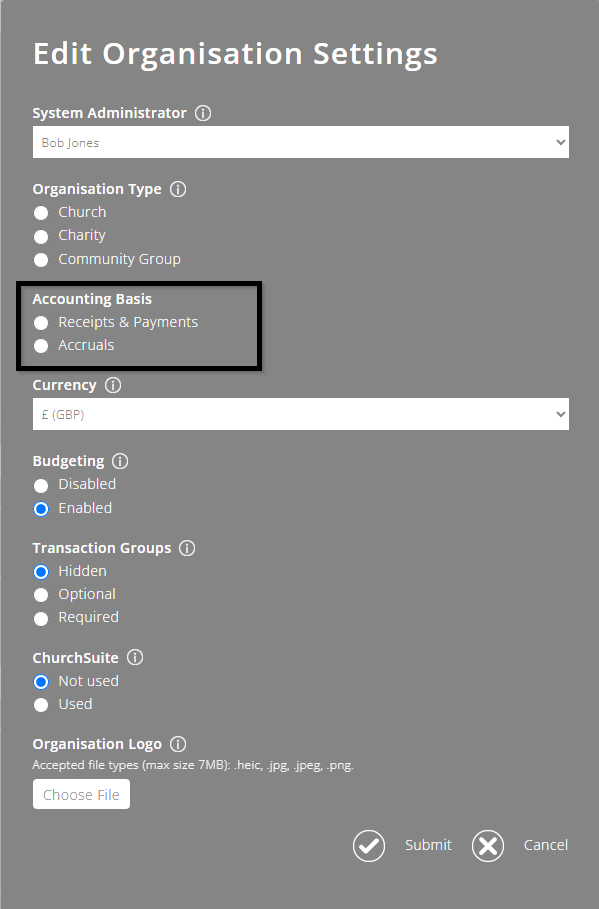

Selecting your accounting basis

When setting up ExpensePlus, you will be asked to select the accounting basis you use to create accounts.

This article refers to various reporting thresholds for the Charity Commission in England and Wales. At the time of writing, some of these thresholds are different in Scotland, Northern Ireland and elsewhere.

There will be a change to these thresholds from 30 September 2026. After this date, the Charities SORP (Charities Statement of Recommended Practice) will have new rules with updated thresholds. If you are not sure, contact your independent examiner or charity regulator.

To learn more about these reporting thresholds and changes, see this blog article on charity accounting threshold changes 2026.

If you are unsure as to what accounting basis your organisation uses, here are two factors that might help you to know:

(1) Size of income - Under UK law, charities in England and Wales with an annual income over £250,000* (this will be increasing to £500,000 for financial years ending on or after 30th Sept 2026) must create end-of-year accounts on 'accruals' basis. Charities with an annual income of under £250,000 usually (but not always) create 'Receipts and Payments' based accounts (also called 'cash' basis).

(2) Type of accounts - If you are unsure about whether your organisation prepares accounts on an 'accruals' basis or on a 'receipts and payments' basis then you should be able to find this out by looking at your prior year's accounts.

This blog post explains more about accounting on a receipts and payments versus an accruals basis.

Receipts and payments accounts

Charities with an annual income below £250,000* are often able to prepare simple Receipts and Payments accounts (as long as they are not charitable companies). Receipts and Payments accounts are a simple form of accounting that consist of a summary of all monies received and paid via the bank and in cash by the charity during its financial year, along with a statement of balances.

If you create accounts on this basis, your year-end accounts may look something like this (or simpler).

Accruals based accounts

Charities with annual income over £250,000*, or that are charitable companies, need to prepare accruals based accounts that comply with the Charities SORP. Accounts prepared using the accruals basis allocate the costs or income of a particular activity according to when the liability is incurred, or when there is entitlement or certainty about income. This is not necessarily the date on which money is received or paid out.

If you create accounts on an accruals basis, then your year-end accounts are likely to look something like this. As you will see, they are far more detailed than simplified receipts and payments based accounts.

If your accounting basis is 'accruals' you will have the option to decide whether or not to enable auto-accruals. Typically we'd recommend you do enable auto-accruals.

Frequently Asked Questions

What if I'm still not sure about which accounting basis to select?

If you do not have prior year accounts, then good people to ask are:

- Your independent examiner - if the gross yearly income of your charity is over £25,000* (this will be increasing to £40,000 for financial years ending on or after 30th Sept 2026) , then you need your accounts to be independently examined, and your Independent Examiner could well be the best person to ask.

- An accountant who understands fund accounting - someone who is a qualified accountant may not necessarily know much about fund accounting (which is different from creating business accounts).

- Someone with experience in creating charity accounts - if your organisation is affiliated to or has contact with people in other charities, chances are that there will be someone who you can approach for advice.

- Stewardship (Christian Charities and Churches) or ACAT (Association of Church Treasurers) - if you are a church or a Christian charity, these two organisations come highly recommended. See their websites for details or contact them to access the services they offer. There may be other organisations that offer help, advice, and training in your local area.

- Charities Commission Website (e.g. Charity Reporting Essentials) - the Charities Commission website has lots of resources, some of which are accessible to everyone, some of which require knowledge of fund accounting.

Find out more here about creating year-end accounts in ExpensePlus.

What does setting my accounting basis do within ExpensePlus?

Receipts and payments accounts are a simple form of accounting. If you select receipts and payments as the accounting basis, the following modules within ExpensePlus are hidden:

- Loans - with receipts and payments accounting, loans are treated as 'income' and repayments as 'expenditure'. At year-end, the outstanding value of a loan is stated as a liability within the Assets & Liabilities statement.

- Investments - with receipts and payments accounting investment gains and losses are not recorded. At year-end, the current investment value is stated as an asset within the Assets & Liabilities statement.

- Fixed Assets - with receipts and payments accounting, asset purchases are simply treated as 'expenditure'. At year-end, the current asset value of any larger fixed assets is stated within the Assets & Liabilities statement.

- Creditors & Debtors - with receipts and payments accounting, transactions are accounted for based on when transactions appear on your bank statement. Therefore you shouldn't be accruing or deferring income/expenditure, and so the option to do this within the adjustments screen is hidden.

If you select accruals as your accounting basis, all the above modules be visible. ExpensePlus will also automatically accrue for any customer invoices you create and any purchases that you enter, removing the need for you to manually add accruals at year-end. This is called auto-accruals. You do have the option to disable the auto-accruals functionality (but we do not generally recommend this).

The accounting basis you select must match the accounting basis on which you will be creating accounts at year-end.

What if I need to change my accounting basis?

If you are just starting to use ExpensePlus and you accidentally selected the wrong accounting basis on the initial pop-up, go to Organisation Settings to change your accounting basis and then make this change in your opening balance setup.

If you need any help or you can't change it yourself as receipts and payments is greyed out, please do get in touch using the yellow 'Send us a message' button at the top of this page.

If you are planning to change the accounting basis for your year-end accounts, you can learn more here about changing your accounting basis and doing this within ExpensePlus.